Field Training Presentation

10 Live Field Training Presentations Are Required

BEFORE SHARING SCREEN

GET TO KNOW THEM, BUILD RAPPORT & TRUST: (About 5 minutes)

●Family / Occupation / Recreation / Where they are from, etc.

○*Your goal is to find something in common in order to build trust*

●Also share a little about yourself as well

(TRANSITION INTO PRESENTATION)

Mr/Mrs. Client, so what has (trainee) told you about our firm, or are you completely in the dark?...In the dark? (haha) no problem at all, then let's turn the lights on for you (haha),

how does that sound? ...fantastic.

So We typically do these trainings for 3 main reasons:

1) To gain support for (trainee) because this is a new career path, and the more support you have in anything, the better off you’ll be

2) For (trainee) to learn how to properly represent our firm, so as we go over everything today, please feel free to ask questions because it will help with their learning curve

and then last but not least...

3) so that If you happen to come across anyone who would benefit from this information, you now know what (Trainee) does, and can have confidence sending referrals

So out of respect for your time, may I ask you a couple of questions in order to tailor today’s conversation?

●Are you actively contributing to any investments or retirement accounts? (IUL)

●Do you happen to have any retirement accounts from a previous employer? (Rollover)

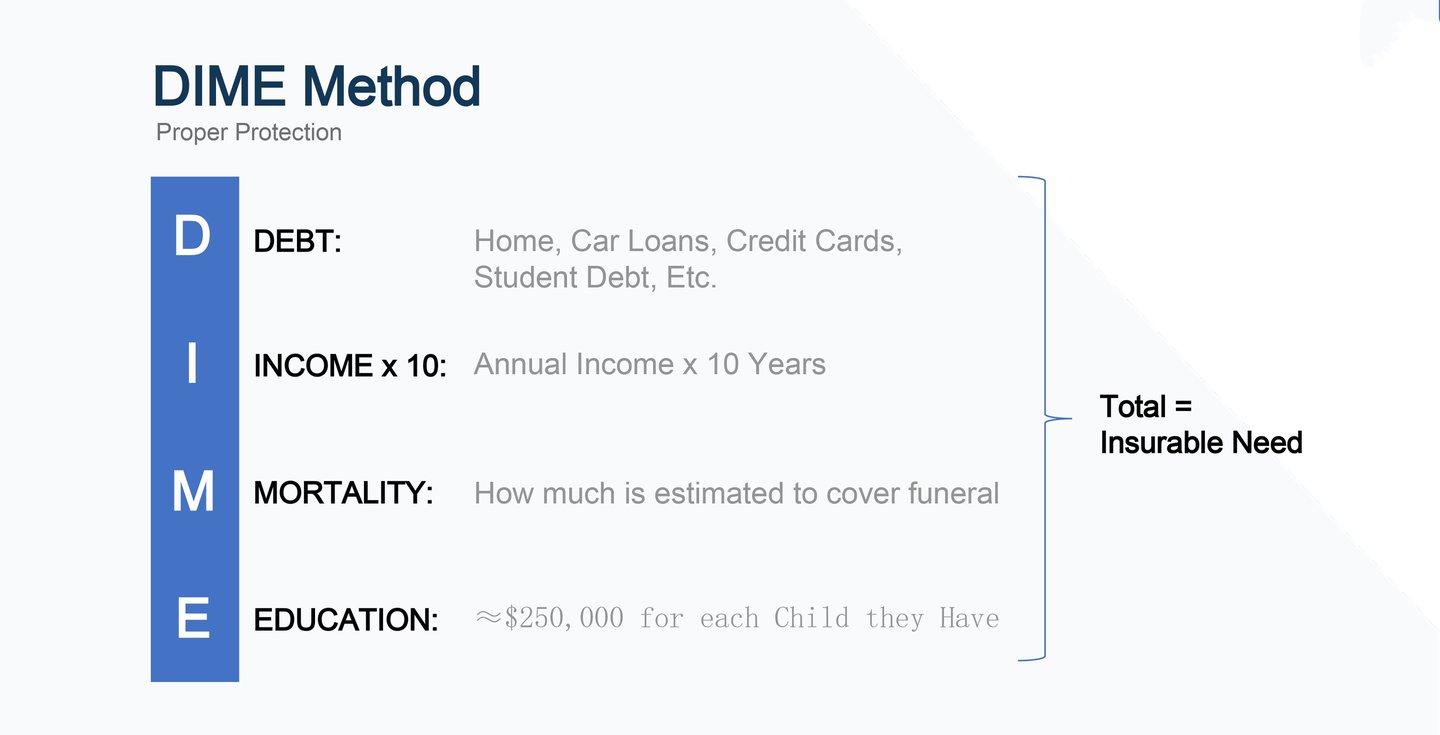

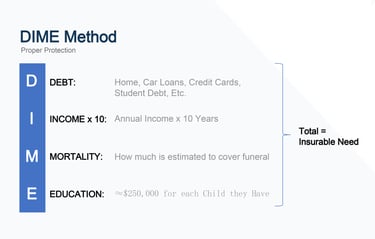

●Are you actively contributing to any type of college fund for your kids? if not, is that something that would be important to you? (Million Dollar Baby)

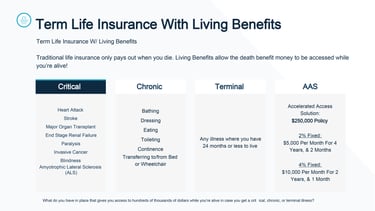

●Do you happen to have an income replacement plan? (Illness or Passing Away) (IUL / Term LB)

START SHARING SCREEN NOW

(CREDIBILITY)

Our company is Global Financial Impact and our goal is to inspire families to dream again.

We’re in partnership with ETHOS. ETHOS is ranked by Forbes as the #1 life insurance company in the United States for 2024.

•ETHOS is backed by Sequoia Capital & Soft Bank, who are some of the largest (if not the largest) venture capitalist companies in the world

We are in partnership with over 25 A-Rated Fortune 500 Financial Institutions.

We are leading the industry in persistency and what that means is when we help a client, they stay on the books with us long term. And can we both agree from an integrity standpoint, that’s very important?

We are licensed in all 50 states, Puerto Rico, Canada, the Virgin Islands & 33 Countries

& Our mission is to help 100 Million families by 2030, which is why i fell in love with the firm and am so passionate because that means that I am able to help families like mine….

Insert 2 minute personal story on why you believe in financial literacy

And one of the reasons we are able to sit down and help a wide variety of families is because we are what you would call a non captive company, by any chance do you know the difference between captive and non captive?

(STRENGTH IN SELECTION)

-A captive company only offers their own products

-As a non captive company, we work with 75% of all the multi billion-dollar fortune 500 financial institutions in North America

-Because we can do pretty much anything when it comes to money, we sit down with a family, provide education, find out their goals, then become their broker and go find the company and or companies that specialize in exactly what they are looking for, does this make sense?

-Not only that, everything we do for a family is complementary. We don’t charge the family, we actually charge the company for bringing them a client they wouldn’t have without us, creating a win-win-win scenario

●Win for the client because they now have 24/7 access to a team of financial specialists that can help them with anything when it comes to money. Not only now, but over the years to come

●It’s a win for the company because they gained a client that they wouldn’t have without us

●And it’s a win for the agent because they are able to sit down with families having no agenda and feel amazing about what they do.

Does this make sense?...excellent

(TRANSITION):

So even though we offer a variety of different products and services one thing that we are big on is taking an educational approach.

So we like to teach our clients the 3 rules of money, by any chance have you ever heard of the 3 rules of money?

NEXT SLIDE

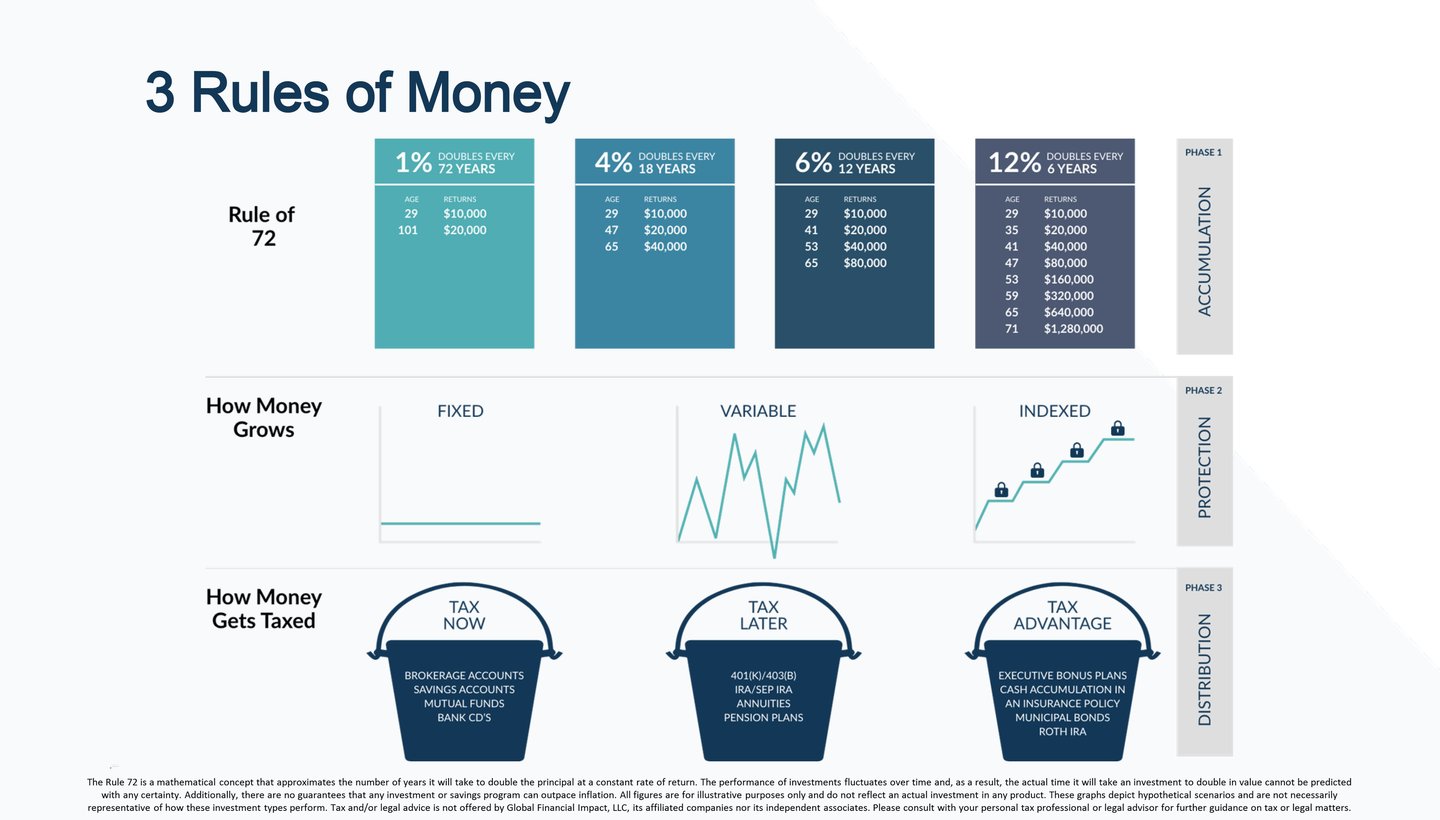

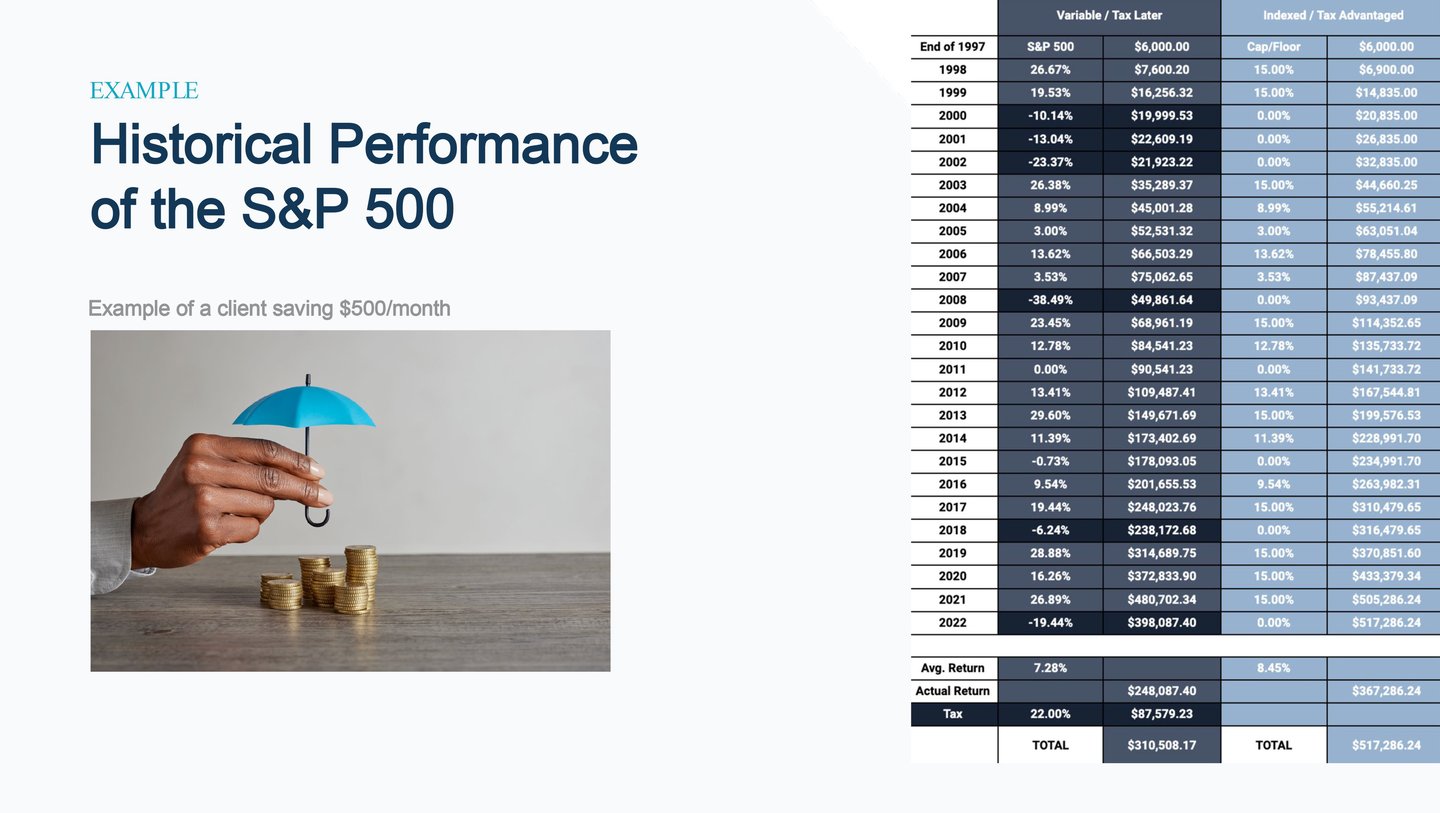

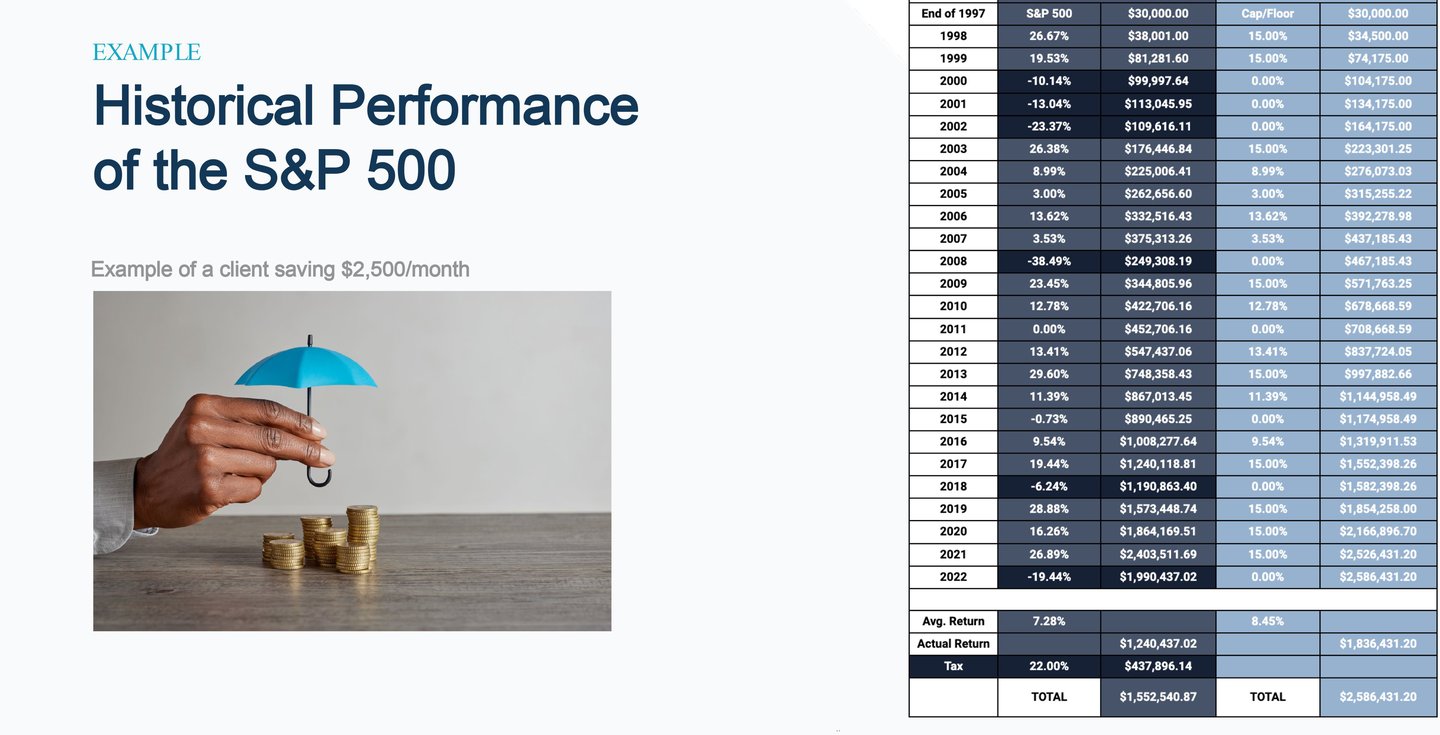

The Rule 72 is a mathematical concept that approximates the number of years it will take to double the principal at a constant rate of return. The performance of investments fluctuates over time and, as a result, the actual time it will take an investment to double in value cannot be predicted with any certainty. Additionally, there are no guarantees that any investment or savings program can outpace inflation. All figures are for illustrative purposes only and do not reflect an actual investment in any product. These graphs depict hypothetical scenarios and are not necessarily representative of how these investment types perform. Tax and/or legal advice is not offered by Global Financial Impact, LLC,its affiliated companies nor its independent associates. Please consult with your personal tax professional or legal advisor for further guidance on tax or legal matters.

Before we dive into the financial education, if you don’t mind me asking, where would you rate yourself on a scale of 1-10 for your general financial knowledge?

Okay, so our goal is for this information to bring some value and potentially bump that number up a little higher, does that sound good?.. awesome!

(RULE OF 72)

So the first rule is the rule of 72. Have you ever heard of the rule of 72? No problem,

Albert Einstein actually considered it to be the 8th wonder of the world and so to give you an idea of how this works, if you take the number 72, and you divide it by the interest that you are earning on your money, thats how long it will take for your money to double

So let's say you're 29 years old and you invest $10,000 into an account that earns 1% interest. 72 divided 1 = 72 which means it will take you 72 years to double your money. Do you have 72 years to wait for your money to double?...me neither!

At 4% your money would double every 18 years, at 6% your money would double every 12 years, and at 12% your money would double every 6 years, getting you to almost $1.3 Million by the age of 71

So when somebody tells me they're saving money, that’s a great thing! But I always ask the question, where? Because if I'm saving $500 in an account that's giving me 4% interest and you're saving $500 in an account that's giving you 12% interest, obviously the 12% interest is going to be better for someone's family, correct?

So for us, our goal is always to get families the highest rate of return possible because of how big of a difference it will make in their life. So in order to get a high rate of return we need to contribute our money into the right account which leads me to the 2nd rule of money which is “How Money Grows”

(HOW MONEY GROWS)

The 1st way for your money to grow is a strategy called fixed, which is considered to be safe and guaranteed. This is like your bank account and when was the last time you saw your bank account grow, without you putting money into it?... Exactly.

So it’s great for emergency funds or accessibility, but can we both agree it’s probably not the best account when it comes to trying to accumulate wealth?... Of course not!

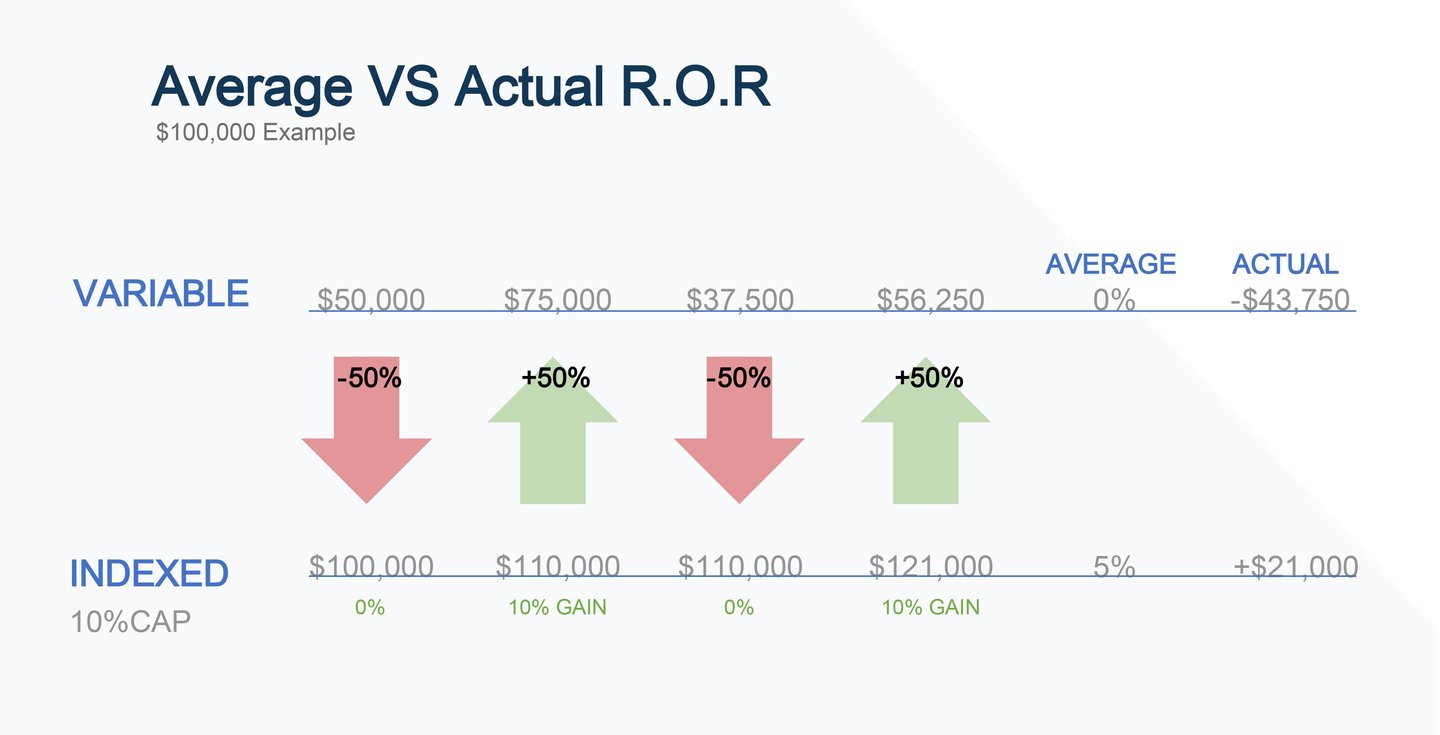

2nd option is variable which is like a 401k, IRA, TSP, or other retirement accounts, typically found through work…

-In a variable account you can make a lot of money, but you also run the risk of, what?….. Losing a lot of money

-And when it comes to your life savings, would you rather have no guarantees or guarantees on your money?...Guarantees, right?

-So Unfortunately, when you have your money in these variable accounts, you don’t even know what your account balance will be tomorrow, do you?...

-So if you don’t know what you will have in your account tomorrow, can you properly plan for your future 10 to 20 years from now?...Of course not,

- so that’s like crossing your fingers and hoping one day to have enough, and that doesn’t sound like the greatest way to plan for your financial future, does it?... Of course not

So is variable bad? No, if you can afford to diversify I would recommend it. but if you are looking for certainty when it comes to your retirement, unfortunately you won’t be able to get that in a variable account

3rd option is a strategy that the wealthy love, which is called indexed growth

Indexed growth gives you the ability to participate on the upside of the market, but if the market crashes you are guaranteed not to lose any principle. So if the market does 8%, then you will earn 8% on your money, but if the market does -8%, your account locks in and you don’t lose a penny.

It is actually public record that this is where banks and 68% of the top 1,000 largest companies in America store and invest their assets. The FDIC (Federal Deposit Insurance Corporation) considers this a tier 1 capital, making it the safest place to have your money

Like I said, if you can afford to diversify your portfolio, we definitely recommend it. However, if a family could only choose 1, which option sounds like the safest way to grow your money?...Indexed?...I would agree!

(HOW MONEY IS TAXED)

So there are 3 different ways for you to pay taxes and as a company we offer all 3….

1st option is called “TAX NOW” which basically means you are going to pay taxes twice. When you get a paycheck you'll pay taxes, and then after the money is invested you will pay taxes on the growth of that money

So the question I have for you, is how much did you like paying taxes the first time?...

Exactly, so let’s move on

The 2nd option is a strategy called “tax later” or most know this as tax deferred, which is normally found through work.

This means you aren’t going to pay taxes now, you will pay taxes later when you go to retire. Which sounds great to people because that means they get to avoid paying taxes upfront. But there are a couple of questions we need to ask ourselves…

1)We don’t get to choose how much we pay in taxes, do we?... Nope

2)and do we think taxes are going down, or can we both agree they are probably going to go up?... Go up, right?

So basically what they are telling families to do, is go work as hard as you can for your money, take your life savings and put it into your 401k (or what they have).

You take on all the risk and liability. Then when you go to retire, the IRS gets to decide how much of your life savings they get to steal out of your account.

This doesn’t sound like the greatest way to pay taxes on your money, does it?...

The 3rd option is a solution that the wealthy have been using for over 100 years which is called tax advantaged

This allows you to grow your money tax free and also withdraw all of the money 100% income tax free

The way this is possible is because when you get paid you have already paid taxes on that money, correct?... Which means you paid your fair share.

So as long as you use the right tax codes and investment strategies, you can actually grow all of your money tax free and withdraw it, once again, 100% tax free

So like I said as a company we offer all 3 and there is a time and place for all of them, but when it comes to your taxes, do you think it would be smarter to pay taxes on the same dollar twice, wait until later, or take the advantage?... advantage, I agree.

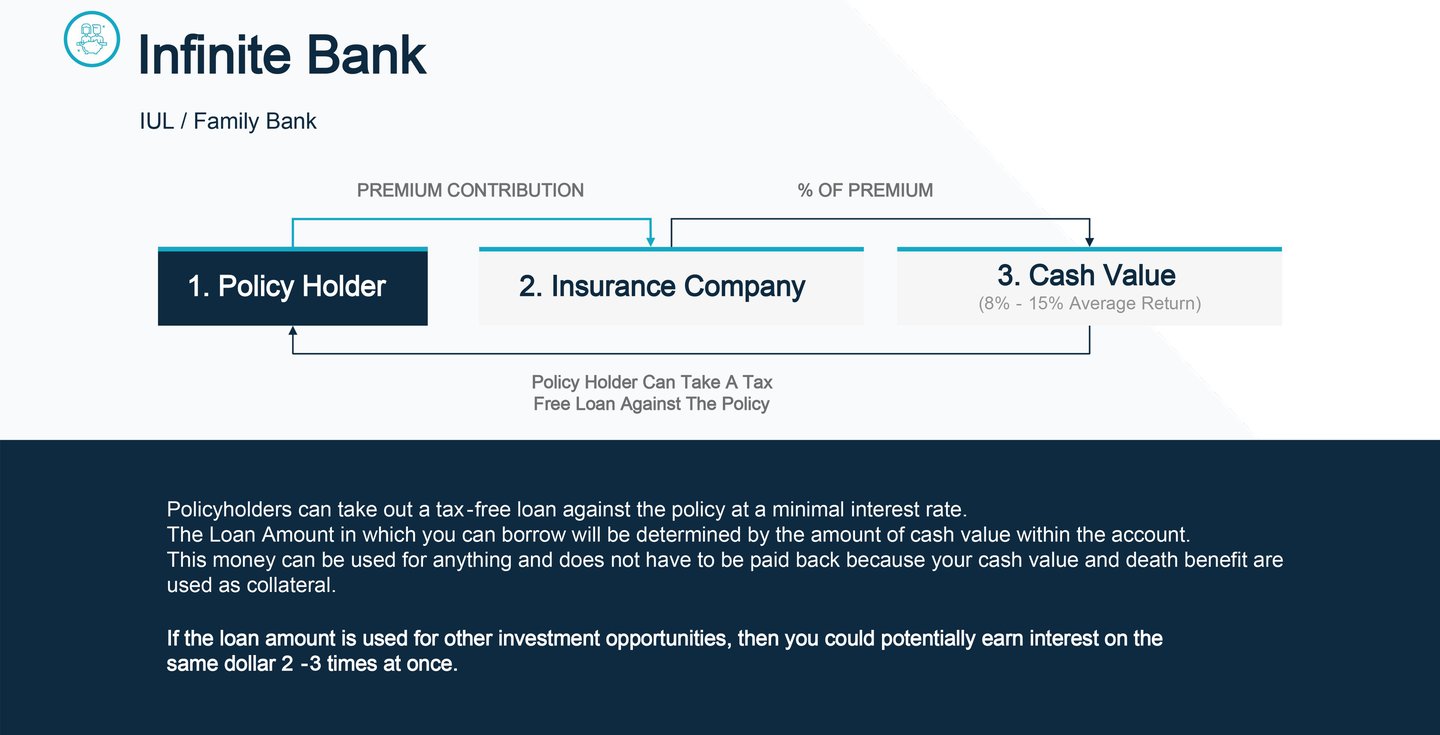

●So since you you were a fan of the Indexed growth and tax advantage strategies, it’s important to know what solutions out there actually give you the ability to leverage your money that way, and only a few do but the wealthy’s favorite program is known as an IUL, Have you ever heard of an IUL? well let me show you why they love it…

NEXT SLIDE >>>

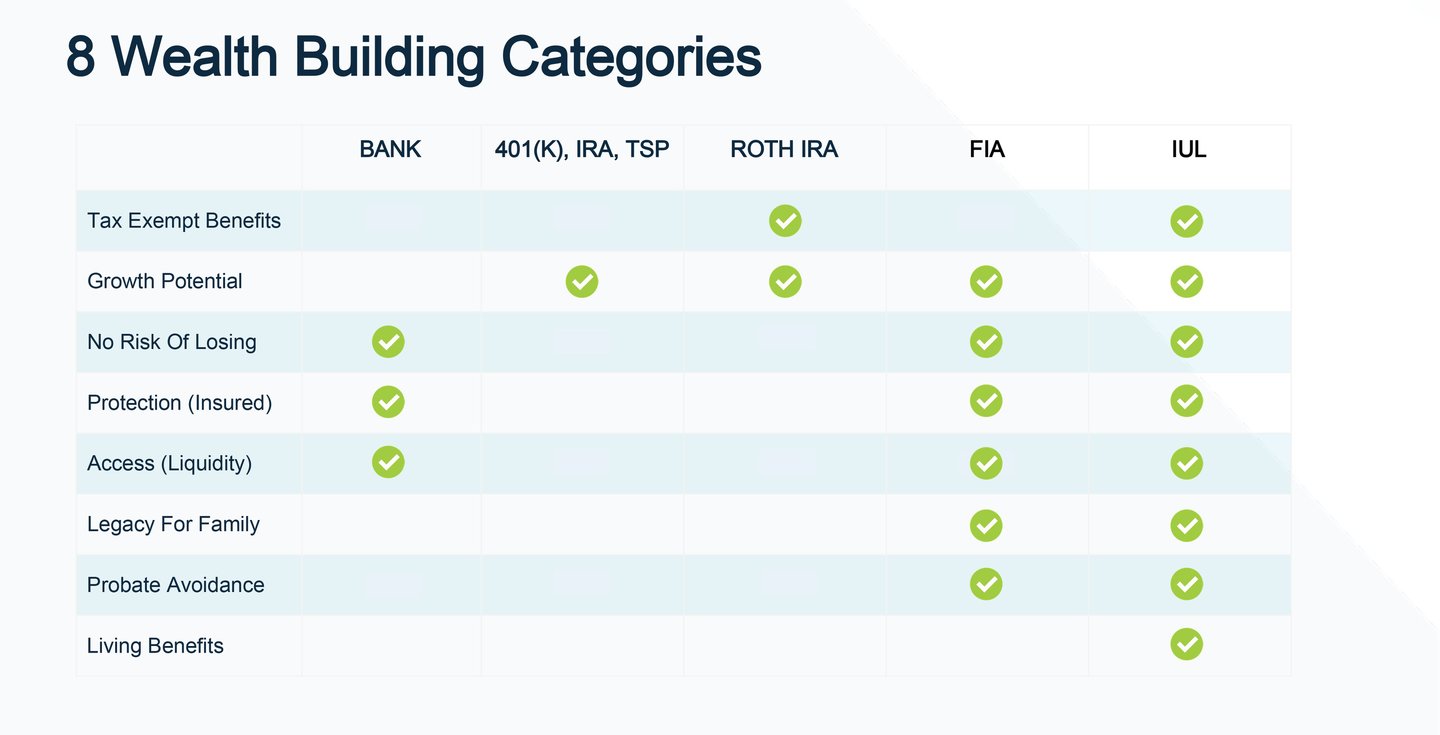

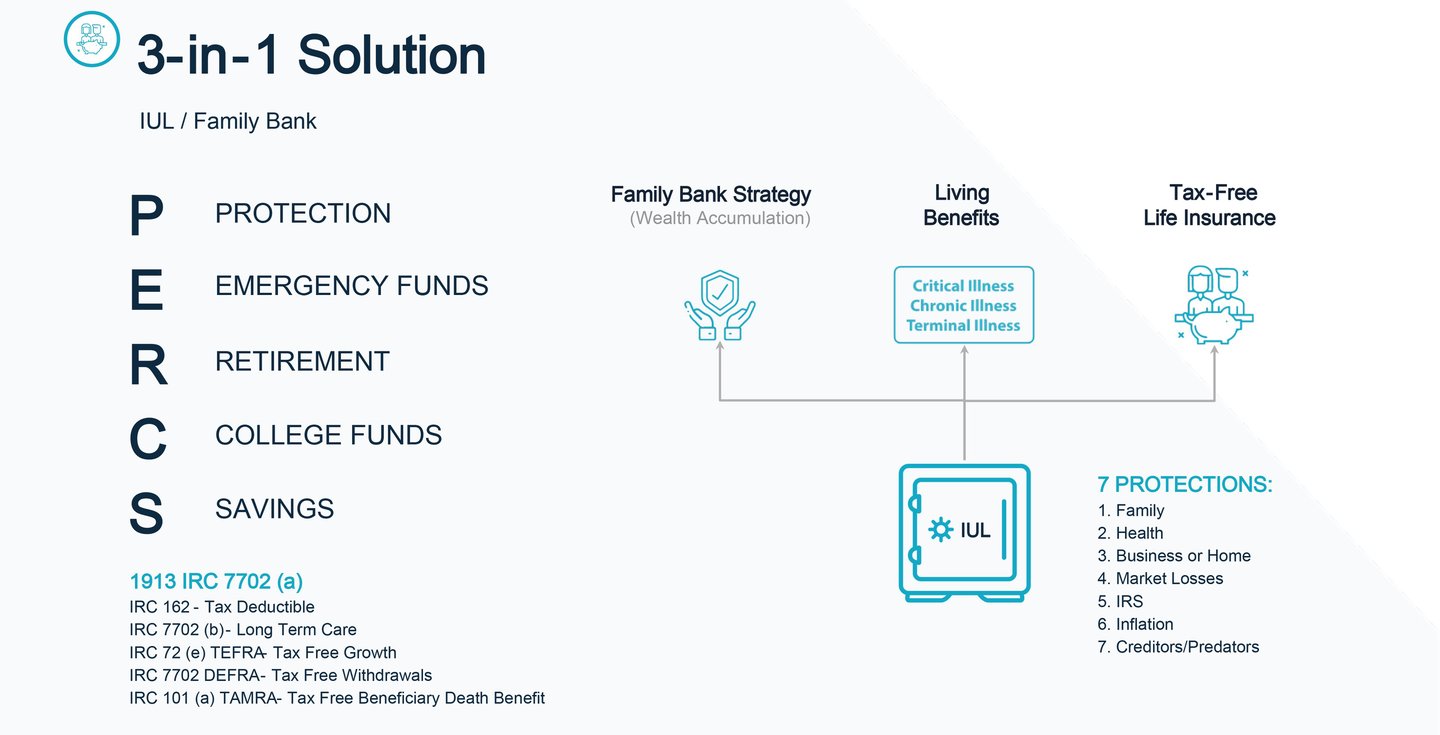

when it comes to building wealth, there are 8 main categories that wealthy people pay attention to

1.As I grow my money - does it grow tax free?

2.Will the account produce high rates of return?

3.Is there guarantees on my money? so if the market crashes my money is safe

4.Is my money insured? so that even if a company is bought, sold, or goes out of business, my money is safe

5.Is it liquid? meaning can I access it?

6.If something happens to me is my family or trust guaranteed to get it?

7.Does it avoid probate? keeping people away that want to fight for my money after I am gone

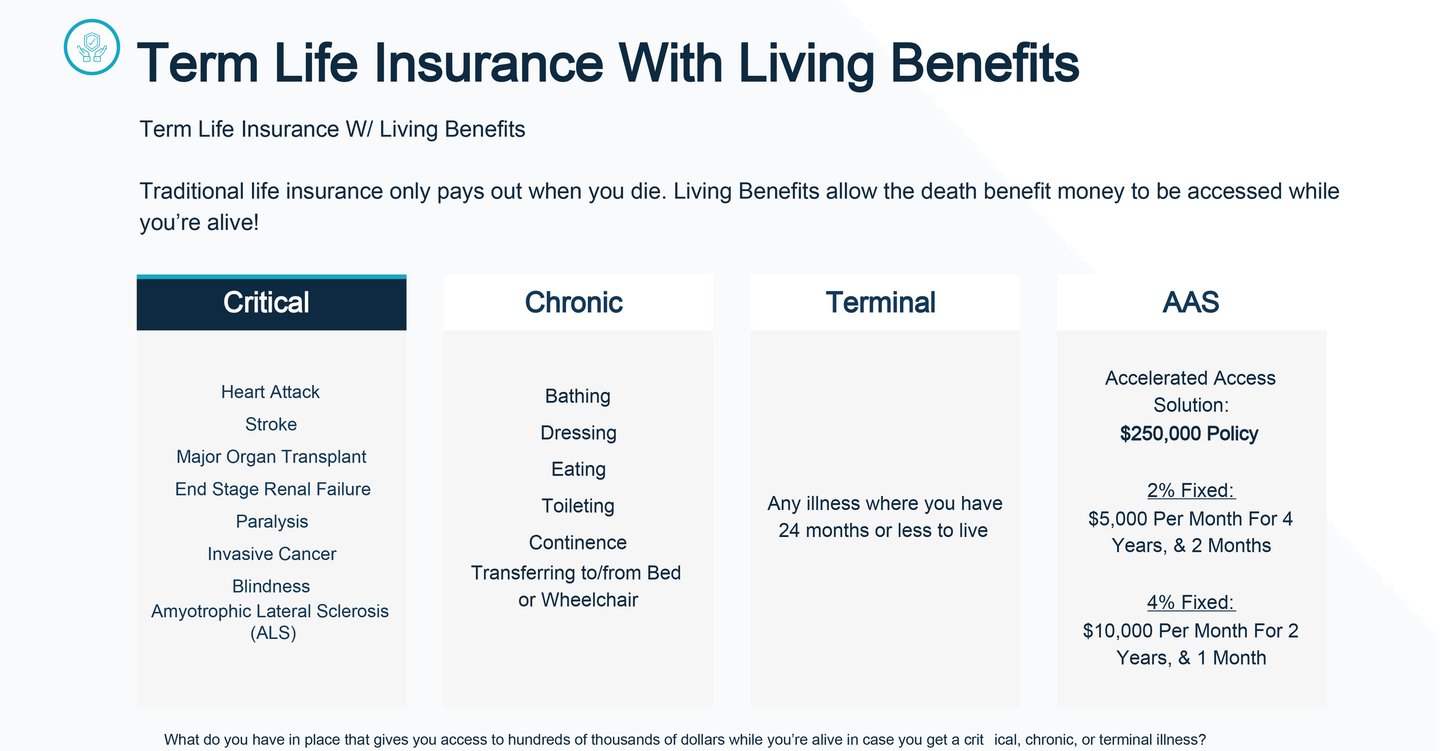

8.Is there illness protection? so if an Illness occurs which more than 76% of americans will experience, I can not only access my money but additional money to take care of my family in that time of need?

so as a company we offer pretty much everything solution on here - but out of all of them, which 1 or 2 solutions do think the wealthy use the most? obviously IUL & FIA right?

So typically… if a family has money sitting in an old retirement or investment account, they will roll it over into the FIA. And then if they are still actively contributing to a retirement or investment account, they will fund that money into a IUL instead. Does that make sense? Fantastic.

So in closing….. NEXT SLIDE

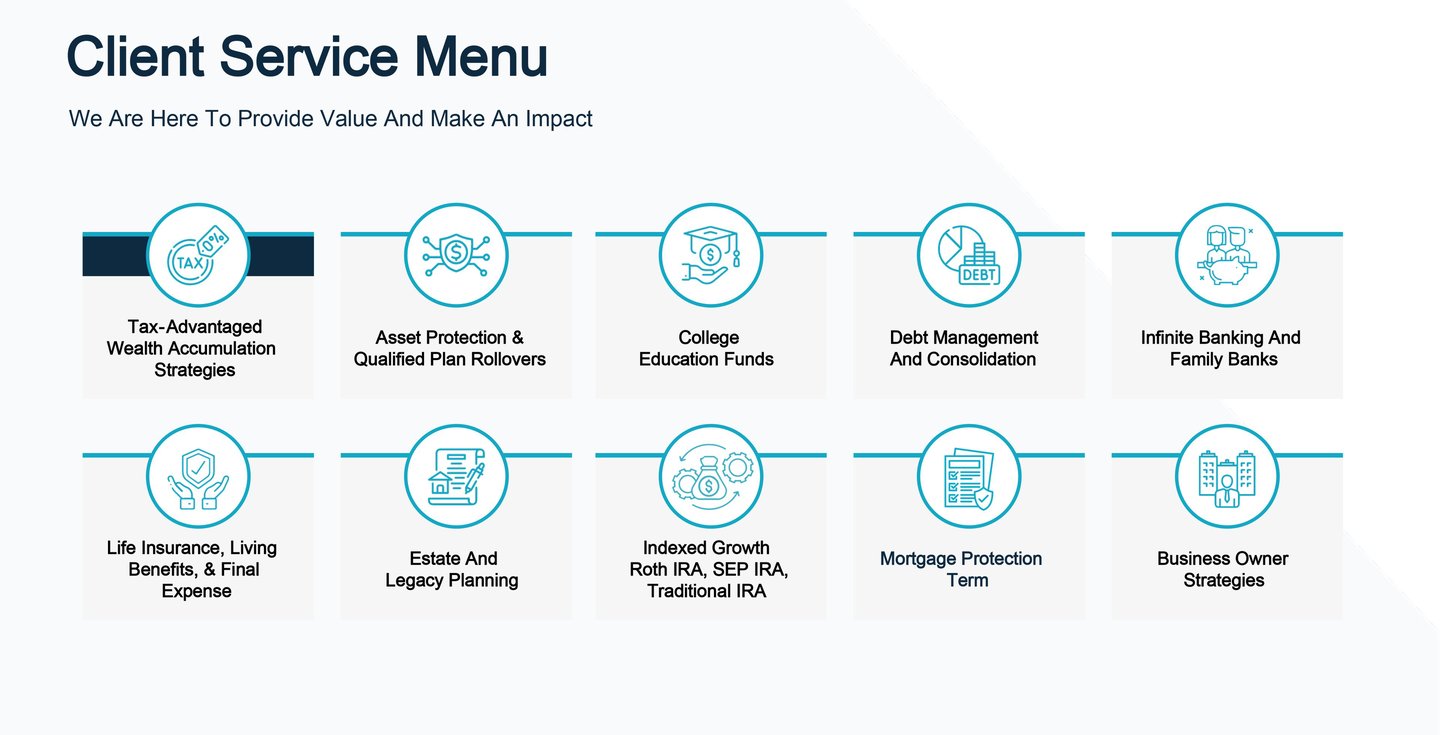

So in closing, there are obviously a lot of different programs and services that we are able to offer in order to make sure that families can have peace in all areas of their finances.

●list them all really quick

So if there were maybe 2 or 3 that you would say are the most important to you and where your family is at, which 2 or 3 would you say are the most important? & why is that?

share a story or connect with them about why those are important and impactful

(TRANSITION: STOP SHARING SCREEN):

As we wrap things up, I want to thank you so much for supporting TRAINEE today for his/her training!

I would love some feedback from you on what stuck out to you the most.. was it how money gets taxed…. or our mission of inspiring families to dream again? What really stuck out?...

Are there any last minute questions you have?...

Would you say that we were able to provide you some value today?... You rated a (*) out of ten, would you say that number jumped up a bit?...

If you don’t have any more questions, if it’s cool with you, I actually have some questions for you.. awesome…

CLOZING QUESTIONS NEXT SLIDE

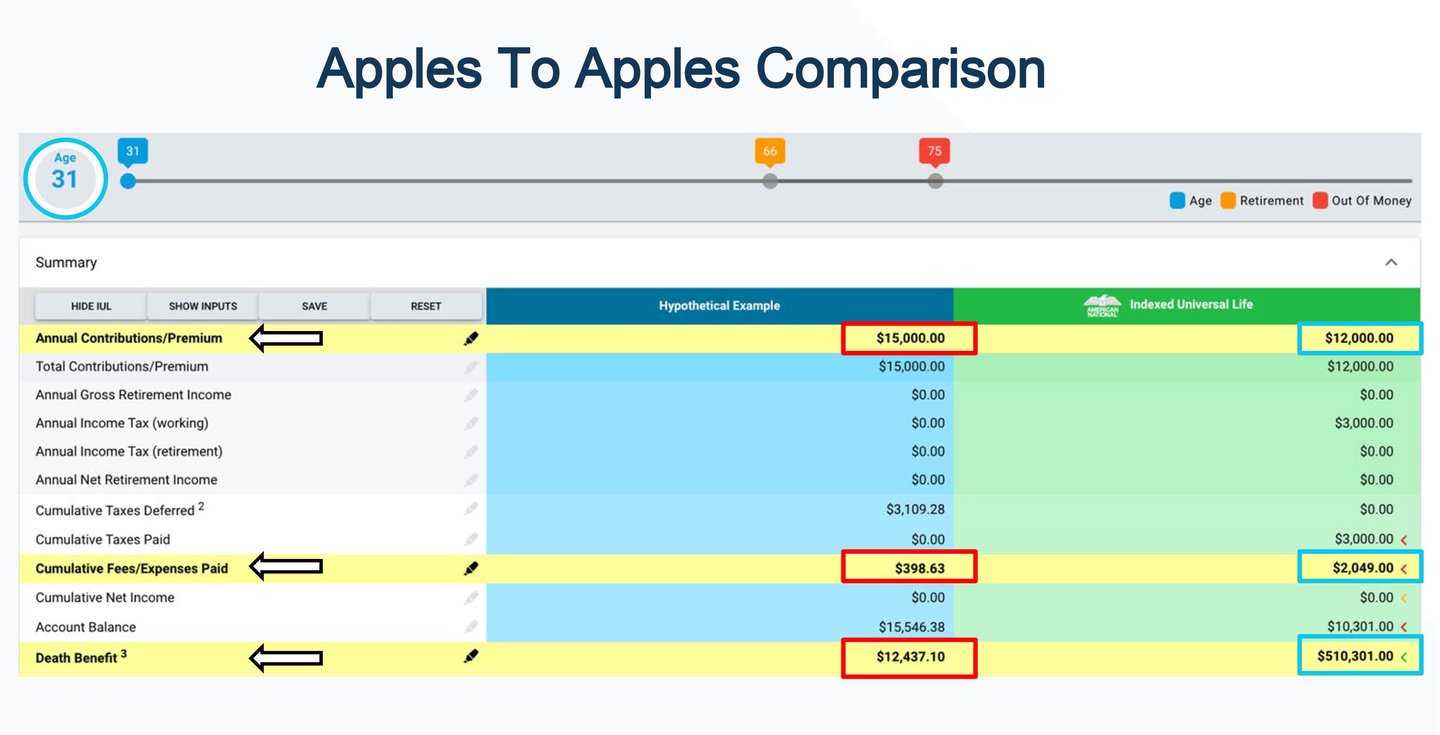

Apples to Apples (Slide 1)

So this is a comparison of the IUL Vs 401k(or whatever they have) which is what most people have been contributing to, and just know that the IUL numbers that you do see here are very conservative because our software is programmed to under promising so we can over deliver

Age 31:

So as you can see in the 401k, you are contributing $15,000 per year, while in your IUL you are contributing $12,000 a year. The reason is because in a 401k you will pay taxes long term, while in an IUL, we are using after taxed dollars in order to insure a tax free retirement solution

I also want to point out that in your 401k you are only paying $398 in fees the first year, while in an IUL you are paying a little over $2,000 in fees. So based off this, the 401k is obviously looking better right? Of course

But what if I told you that

A) over time, your 401k would actually cost you way more in fees, which I’ll show you here in just a second

B) the only reason you are paying a little bit more in fees up front in your IUL, is because if you died today, your family would receive a tax free check for over $510,000 to support them through the worst time of their life... while in a 401k, they would only get $12,000. That’s powerful isn’t it?

And C) because if you got diagnosed with a critical, chronic, or terminal illness, which over 76% of Americans will experience, you could access up to 90% of this $510,000 to support your family through once again, one of the hardest times of their life.

So knowing all of this, Can we both agree, that paying a little more in fees upfront would be worth the peace of mind long term? Of course

And Just curious, do you happen to know anyone that’s ever been diagnosed with an illness and or passed away, and because of it their family struggled financially? Yes? And would you ever want that to happen to your family? Of course not… and this keeps that from happening. isn't that incredible?

NEXT SLIDE

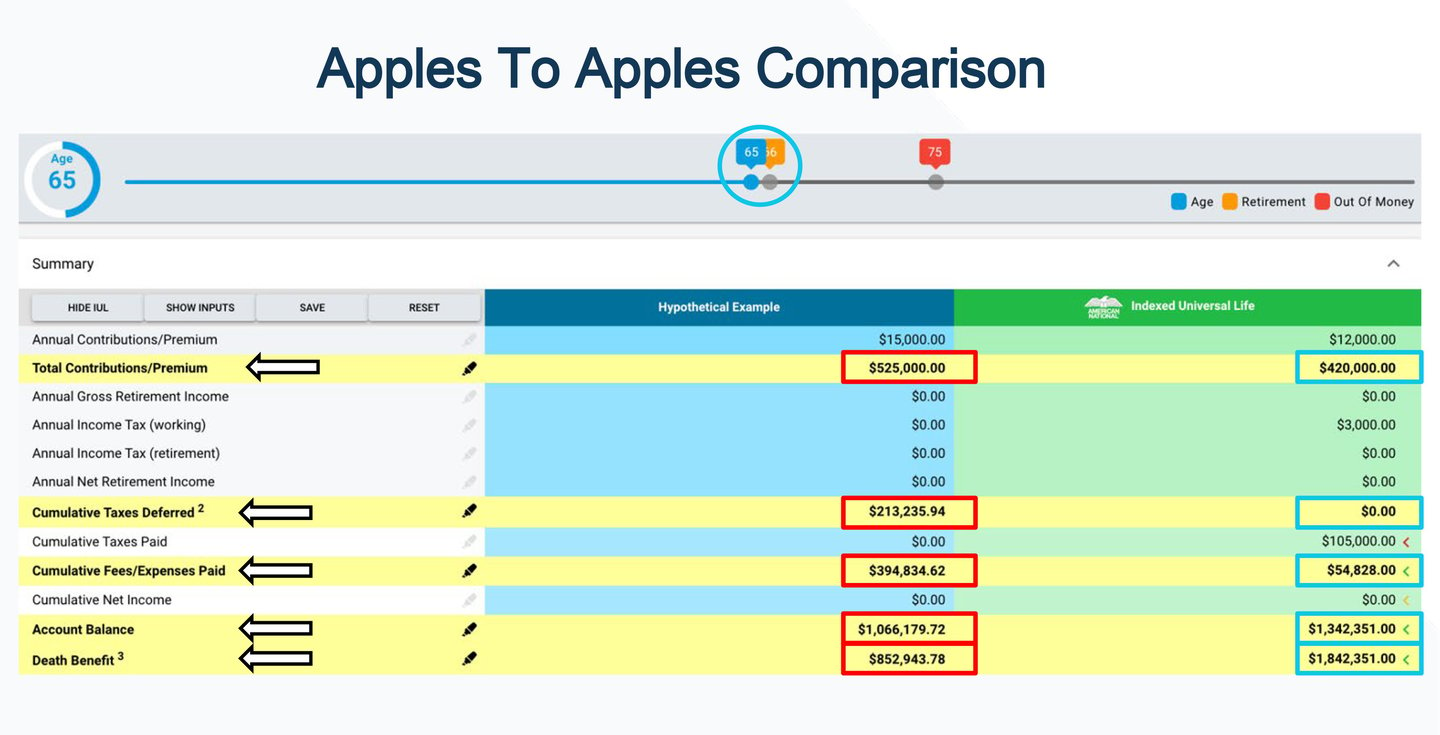

Apples to Apples (Slide 2)

So now we get to the age of 65 years old. And at 65 years old, you contributed a total of $525,000 into your 401k, versus $420k into your IUL.

In your 401k you owe $213,000 in taxes, and in an IUL you owe $0 in taxes.

In your 401k, You have paid about $400,000 in management fees, while in an IUL you only paid $55,000 in fees.

Your 401k account balance would be a little over $1,000,000, while in an IUL, you would have over $1,300,000 TAX FREE.

And if god forbid you passed away at age 65. In a 401k you would leave behind about $850k, while in your IUL you leave behind over $1.8m tax free.

so I am not finished explaining everything just yet, but based off what we have covered, what sounds better to you, the 401k or the IUL? Obviously the IUL

NEXT SLIDE

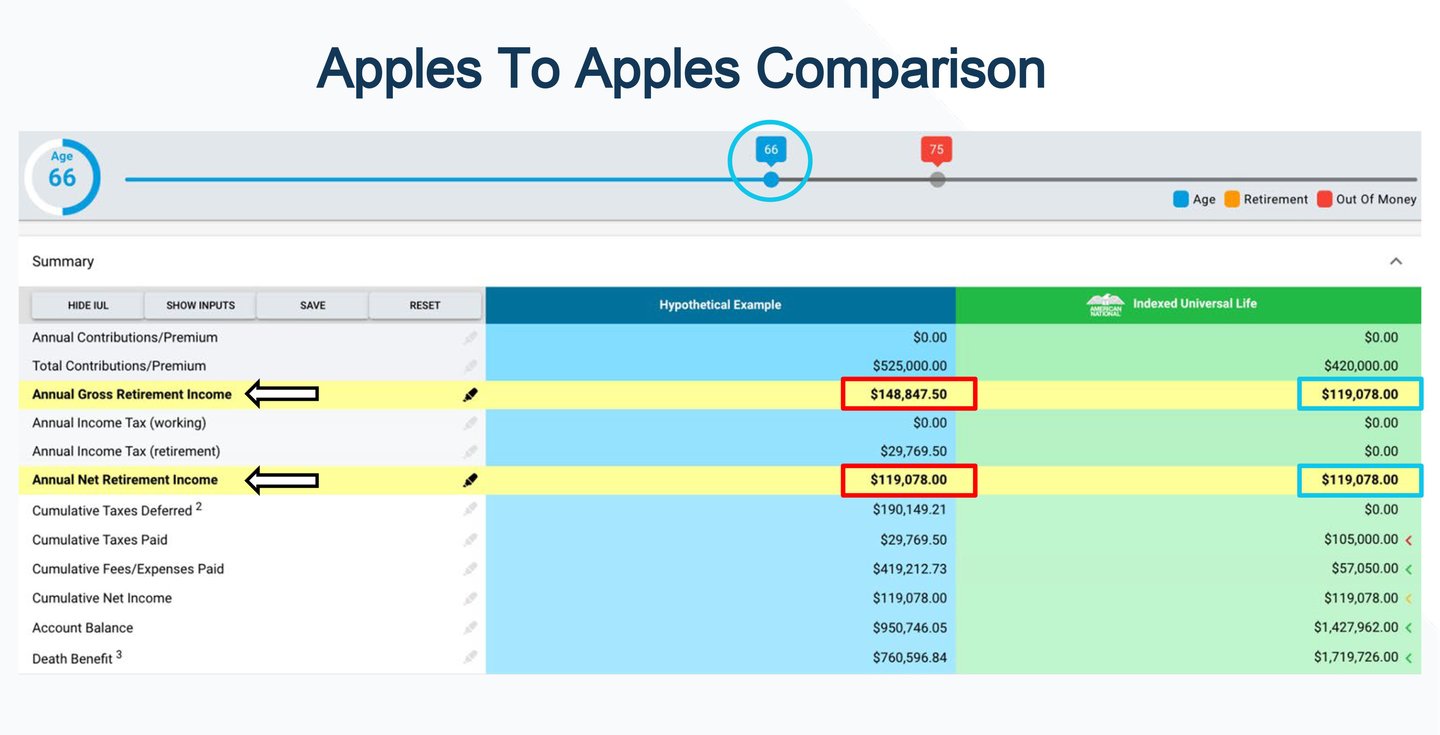

Apples to Apples (Slide 3)

Age 66

So now at age 66 we start taking income, and in your 401k you would have to take out $148k a year, to have a net income of $119k

while in a IUL because it’s tax free, all you have to do is take out $119k to generate the same result.

But in a 401k because it’s taxable income, you are now in a $148k tax bracket which will affect your social security. While in an IUL it’s 100% tax free, which means you are in a 0% tax bracket. So would you rather earn earn $119k a year and be at the highest tax bracket, or make $119k a year, be at a 0% tax bracket, and maximize your social security?

But it’s not just about how much we make, but how long our income lasts. So as I drag the age dial I want you to pay attention to how long your income would last in a 401k versus in an IUL.

NEXT SLIDE

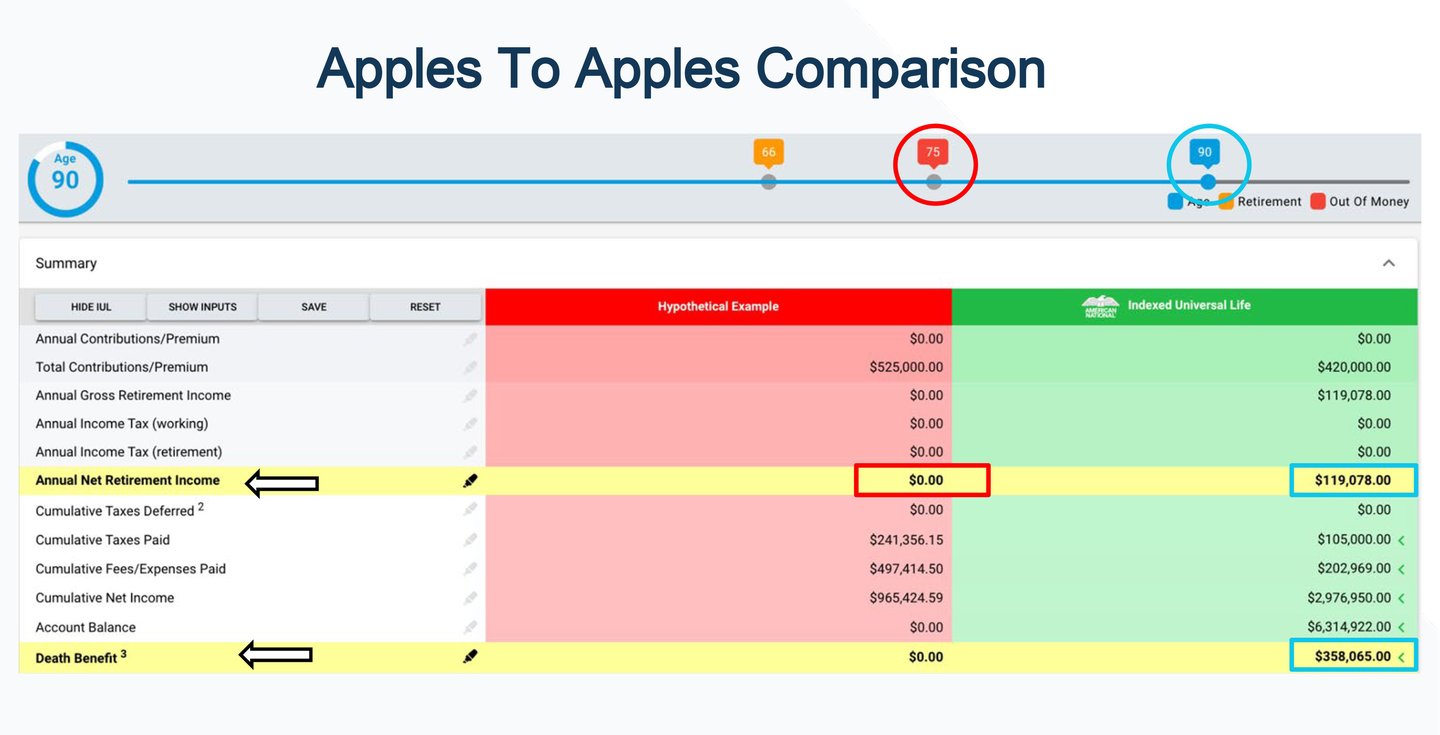

Apples to Apples (Slide 4)

So as you can see at the age 75 years old, you officially ran out of money in your 401k... And at 75, would you rather be submitting Resumes? Or planning your next vacation with family? obviously your next vacation? but unfortunately most people will be submitting resumes because of a lack of education.

so as I drag the age dial, as you can see, your IUL income is set to last until age 90. but keep in mind I can structure this to last as long as you want.

So CLIENT, would you rather run out of money at age 75, or have a tax free income all the way until age 90? Age 90 right?

and what's crazy about this, is that even at age 90, you still have almost $360,000 to pass on as tax free legacy money to your family...

So in an IUL you contributed a total of $420,000, and took out over $3.3M tax free. And so if you wrote us a check for $420k, and we wrote you back a check for $3.3m tax free, would that be a no brainer for you and your family? Of course (HAHA)

So do you happen to have any questions, or does everything make sense to you? Amazing

so one of the things we can actually do is design an entire plan for you if you would like, but we can talk about that later no problem…

GO TO NEXT SLIDE

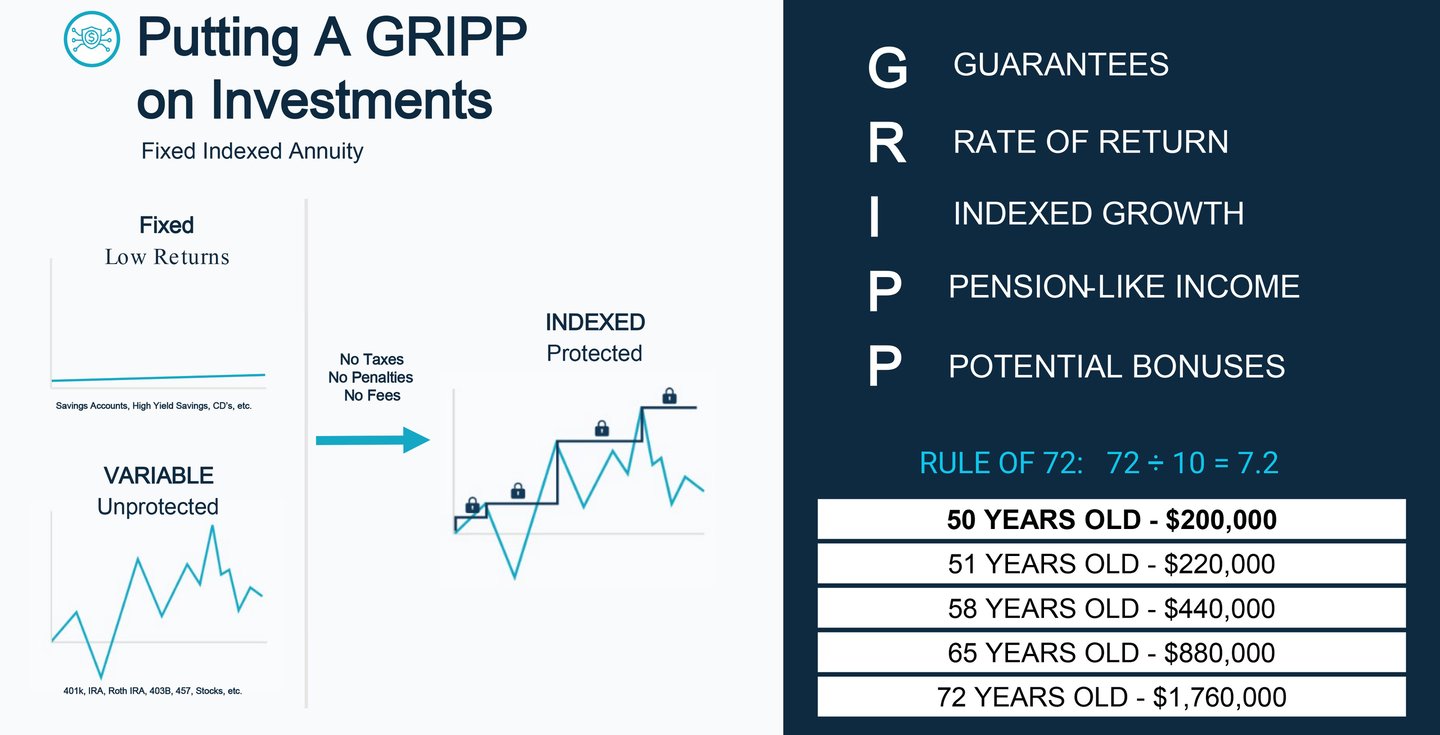

So let's say someone currently has their money in a fixed account where it's losing money to inflation, or, they have their money in a variable account where they can potentially lose it to a market decline.

what we will typically do, is help them roll that money over from their old account into a new and improved account that grows indexed, has guarantees, and we don't charge a single penny to do this....

we call this putting a GRIP on a families retirement account....

The G stands for GUARANTEES, because Mr & Mrs client, would you rather have no guarantees or guarantees on your money?

the R stands for Rate of Return, because would you rather have no guaranteed rate of return, or a guaranteed rate of return?

the I stands for Indexed Growth, because would you rather have your money at risk in the market, or in an account that only participates on the upside of the market and never the downside?

and then the P stands for Pension Like Income, because would you rather have no guaranteed income, or a guaranteed income for life?

So imagine having your life savings in your left pocket, but then finding out there was a hole in it? how fast would you move that money? as fast as possible right? of course. So thats what we do...

We help families move their money from their left pocket, to their right pocket, where it's safe and secure.

does that make sense? fantastic

So if you and your money qualified for something like this, is that something you would be open to? Amazing!

So in closing, there are obviously a lot of different programs and services that we are able to offer in order to make sure that families can have peace in all areas of their finances.

●list them all really quick

So if there were maybe 2 or 3 that you would say is the most important to you and where your family is at, which 2 or 3 would you say is the most important? & why is that?

share a story or connect with them about why those are important and impactful

(TRANSITION: STOP SHARING SCREEN):

As we wrap things up, I want to thank you so much for supporting TRAINEE today for his/her training!

I would love some feedback from you on what stuck out to you the most.. was it how money gets taxed…. or our mission of inspiring families to dream again? What really stuck out?...

Are there any last minute questions you have?...

Would you say that we were able to provide you some value today?... You rated a (*) out of ten, would you say that number jumped up a bit?...

If you don’t have any more questions, if it’s cool with you, I actually have some questions for you.. awesome…

CLOZING QUESTIONS ON SLIDE 22

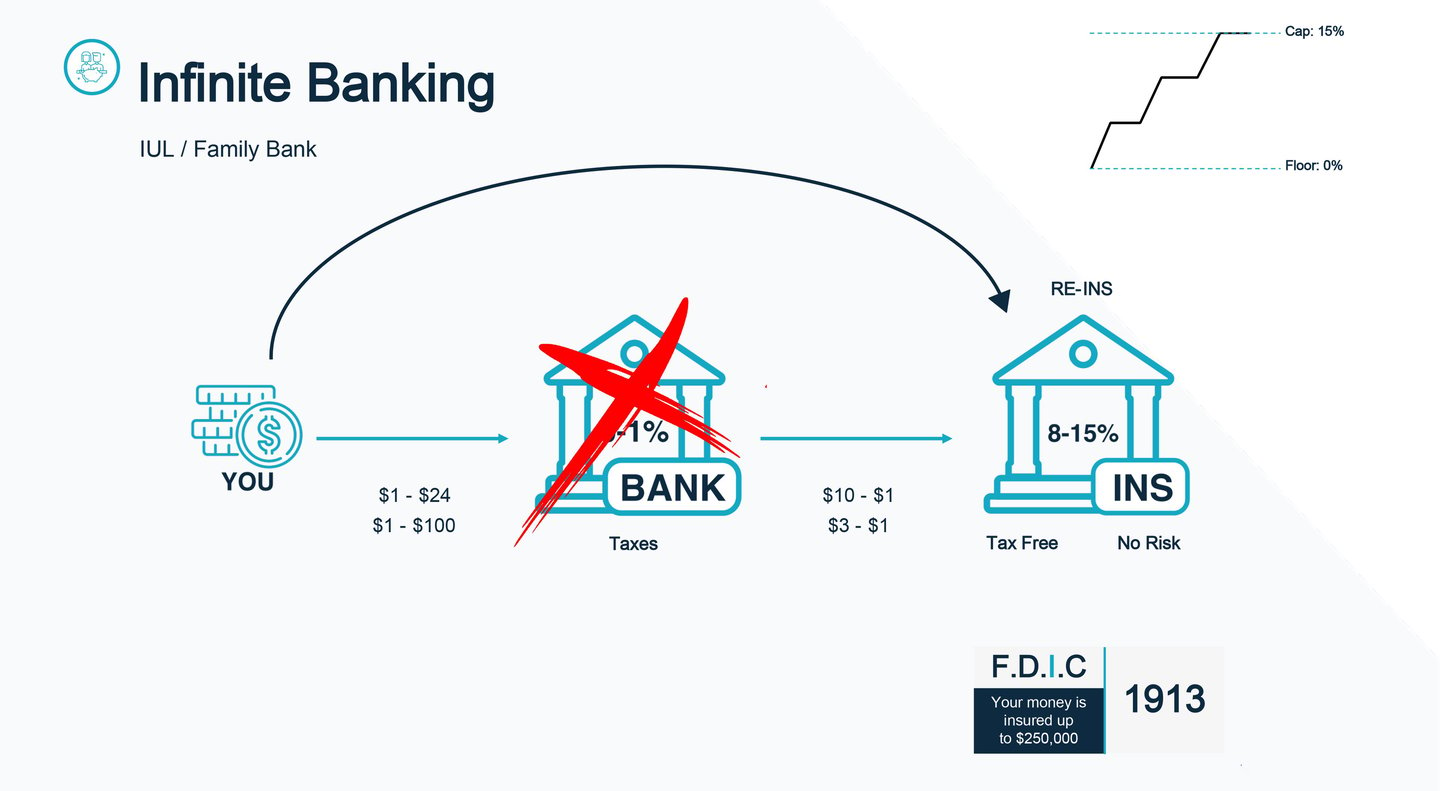

Here’s you*click*. So where do you (and everyone you know) put your money after getting paid? The bank! click

When you give your money to the bank, they’ll give you 0-1% interest on your money. However, on the growth of that money, you still have to pay taxes. click

Now, why do people like the bank?...because it’s safe…*click*...The bank is backed by the FDIC, which is the Federal Deposit Insurance Corporation. They’ll insure your money up to a quarter million dollars.

What most people don’t know is that for every $1 we give the bank…*click*... they can legally turn around and lend out $24. Back in 2008, when the economy crashed…*click* for every $1 we gave them they were lending out $100! Can you believe that!?

So guess what happened...the market crashed, everyone came running to pull their money out and the banks didn’t have it! We had over 500 banks go bankrupt! It was a huge mess, we had all the government bailouts...it was bad.

But here’s the thing...the banks will gamble with our money all day long, but they are MUCH smarter with what they do with their own money…*click*...Banks put as much of their money as humanly possible into life insurance companies. Why do they do this? The FDIC considers this TIer 1 capital which is the safest capital a bank can have. They also get 8-15% of a return…*click*...it’s 100% tax free…*click*...and there’s no risk. How is there no risk?

Because these accounts grow indexed…*click*...meaning that anything between 0 and 15% they get to keep.

The banks also know that these insurance companies have to play by a different set of rules…*click*... Meaning that for every $1 they have in liabilities, they have to have 10 times that in assets! …*click*... If that ratio ever drops below 3-1…*click*...there’s something called re-insurance corporations that come in and cover them until they get back to where they need to be. This is why we’ve NEVER seen a SINGLE life insurance company go out of business in the history of our country. Make sense?

How long do you think the banks have been doing this with our money? Click SINCE 1913!

Most people ask me “Well if this has been around so long why haven’t I heard of this before?” Most people have never met with a licensed financial professional before. So it’s not that it doesn’t exist, we just don’t know about it.

Plus, if the banks are making 8-15% on YOUR money and only giving you 1% in return, do you REALLY think they’re gonna tell you about this? Of course not!

Obviously we still need to have a checking and savings, but when it comes to investing…*click*...we show families how to skip the banks…*click*...and go straight to where the banks are investing our money

So the question is - would you rather the banks make money on your money...or would YOU rather make money on your money…?

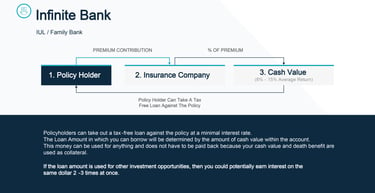

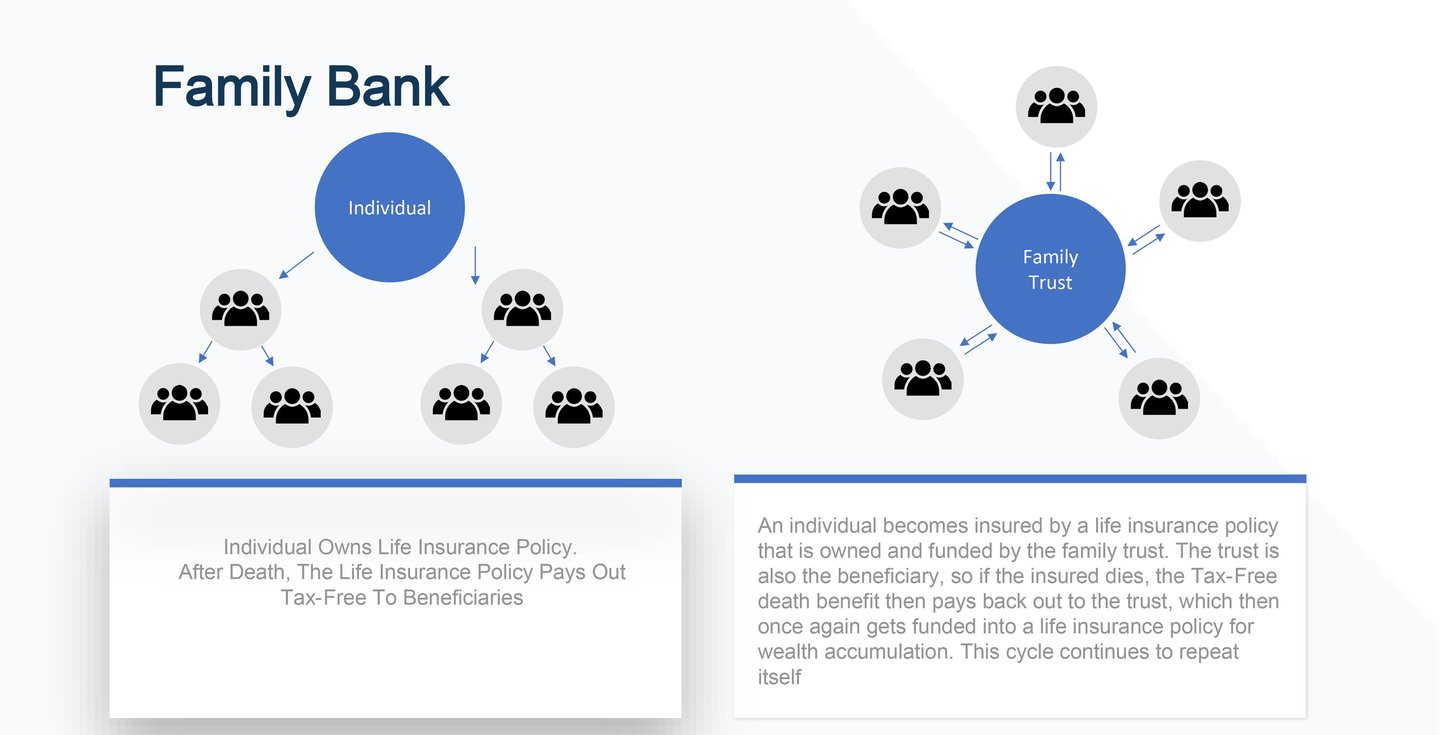

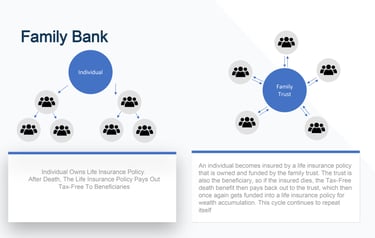

So all we do is teach families how to do what the banks are ALREADY doing with our money, creating your own family bank.

"Protect Today. Build For The Future"

CFI © All rights reserved.